Author: Dinesh Giridhar, Co Founder,Managing Director & CEO - Asset Management & Private Wealth, Dolat Capital

For much of the last two decades, however global equity markets have quietly undergone a structural shift. In the United States and Europe, quantitative and rules-based investment approaches have moved from the fringes to the foundation of portfolio construction. Large pension funds, sovereign wealth funds, and institutional asset managers increasingly rely on systematic frameworks not as experimental overlays, but as core drivers of capital allocation across equities, fixed income, and alternatives. The logic is straightforward. As markets grow larger, faster, and more complex, consistency in decision-making becomes as valuable as insight itself.

India’s evolution has followed a different timeline. For many years, equity investing in India was dominated by discretionary judgment, relationship-driven allocation, and narrative-led decision-making. In a market once characterized by lower participation, limited data availability, and slower information flow, this approach was not only viable. It was effective. Quantitative investing existed, but largely at the margins, constrained by infrastructure, data quality, and market depth.

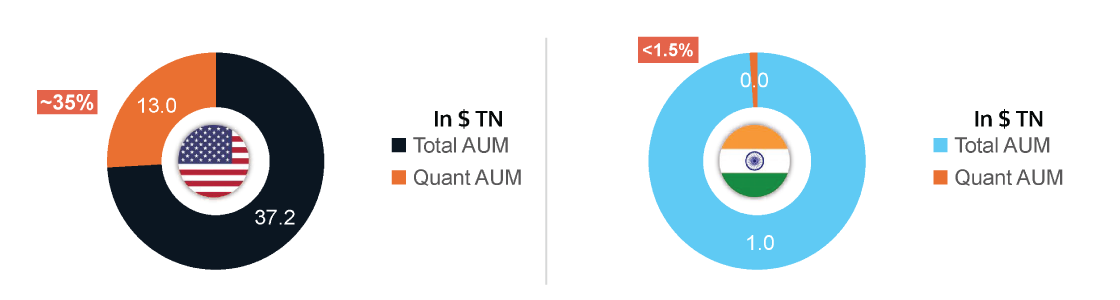

Chart 1: Global vs India Quant Adoption

That context has changed decisively over the last ten years.

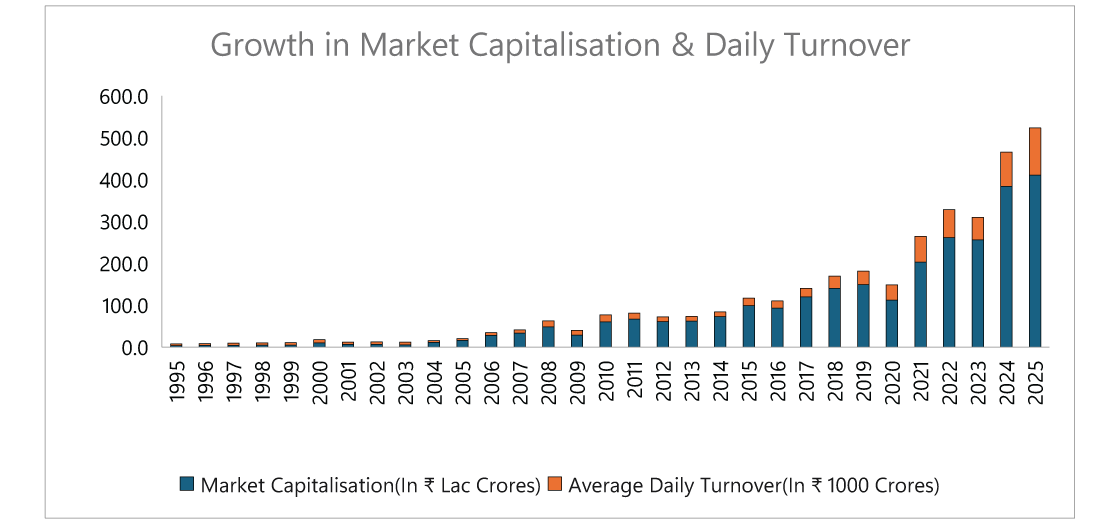

Indian markets today are deeper, broader, and structurally more complex than they were a decade ago. Market capitalisation has expanded materially, institutional participation has increased, electronic trading has become ubiquitous, and data availability has improved dramatically. Regulatory reforms, faster dissemination of information, and rising retail participation have shortened the shelf life of intuition. In such an environment, reliance on judgment alone becomes increasingly difficult to sustain. This is precisely where quantitative investing begins to matter, not as a replacement for market understanding, but as a framework for introducing discipline, repeatability, and structure into long-term portfolio construction.

Chart 2: Growth in Indian Market Depth (1995–2025): market capitalization & average daily turnover

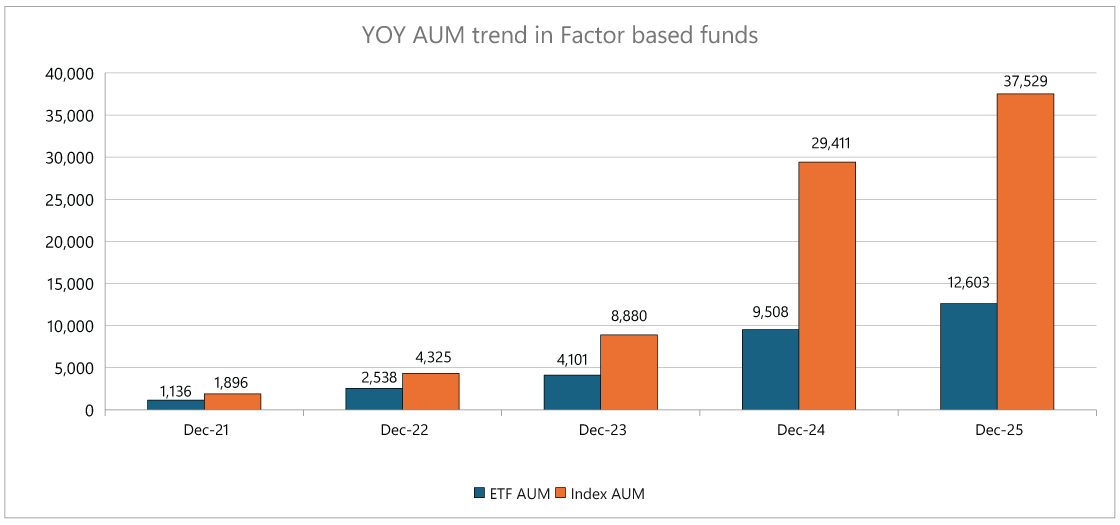

Source: AceMF, all smart beta ETFs/Index Funds and Multi Factor index/ETFs. Data as on 31 Dec 2025.

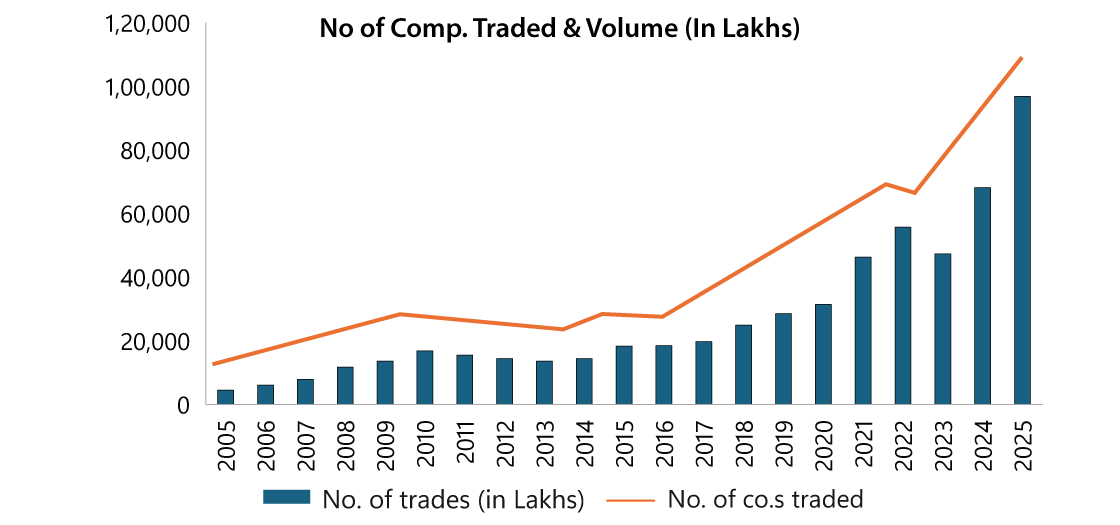

Source: Dolat Internal Research, ACEMF, Bloomberg, NSE, NSDL and MorningStar. Data as on 31 Dec 2025.

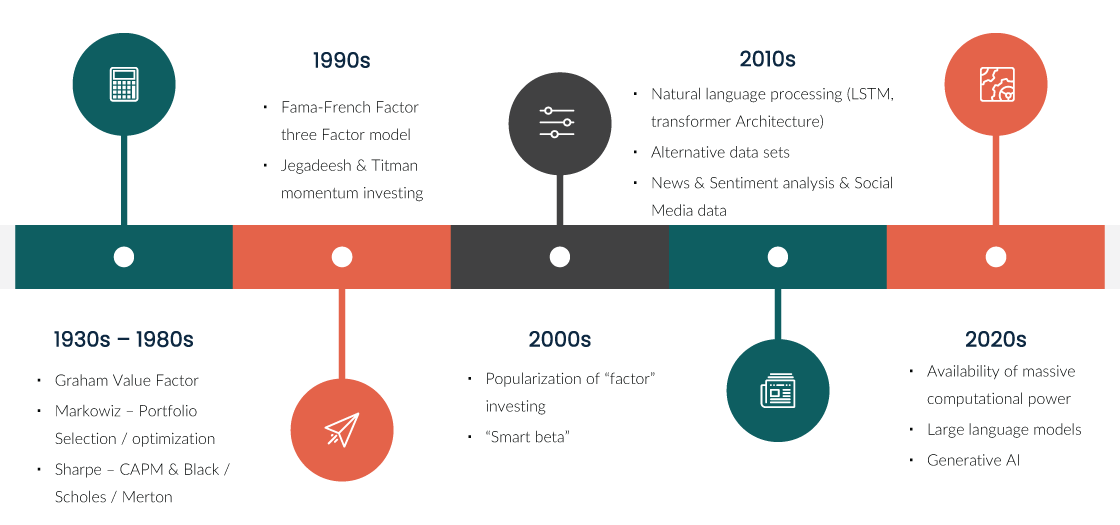

From Academic Curiosity to Portfolio Architecture

Globally, quantitative investing did not emerge overnight. Its roots lie in academic finance, beginning with early work on portfolio theory and statistical inference. In its earliest form, quantitative investing was shaped by constraint. Data was scarce, computing power was expensive, and execution was manual. Models relied on simple rules, ratios, and regression, linear relationships derived from relatively small datasets and tested over short historical periods. Single-factor strategies dominated, and portfolio changes were infrequent.

Yet these early efforts introduced a powerful and enduring idea. Investment decisions could be structured, tested, and improved systematically, rather than driven purely by narrative or emotion. Quantitative investing did not begin as a quest for complexity. It began as a search for discipline.

The intellectual foundations laid during this period continue to influence modern quantitative frameworks, even as tools and techniques have evolved dramatically.

When Technology Changed the Rules and Raised the Bar

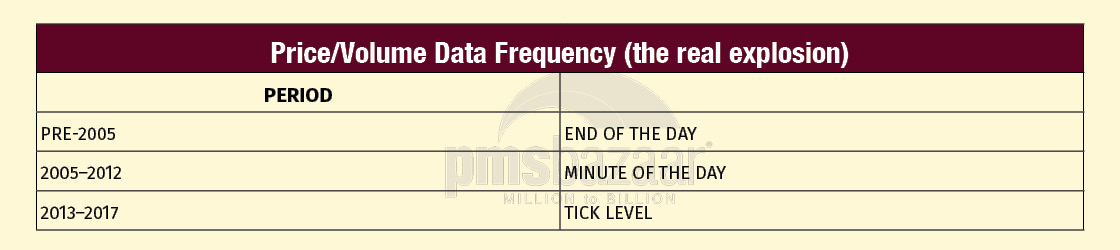

The true inflection point for quantitative investing came when technology finally caught up with theory. Over the past decade, advances in computing power have transformed how investment ideas are researched, tested, and deployed. Multi-core processors, cloud infrastructure, and parallel computation now allow strategies to be evaluated thousands of times across assets, time periods, and market regimes.

Two decades ago, computational constraints shaped quantitative investing as much as intellectual frameworks. In India, research environments were limited by on-premise infrastructure, high computing costs, and minimal parallel processing. Strategy development had to be selective: backtests were narrow, histories were short, and stress-testing across regimes was often impractical.

As hardware costs fell and cloud adoption began in the mid-2010s, these constraints eased. Broader datasets, longer histories, and multi-factor models became feasible, though still constrained by capacity. Today, elastic cloud computing and large-scale parallel processing have fundamentally expanded the research frontier. Strategies can be tested across decades and regimes within hours, shifting the bottleneck from computation to judgement.

This shift has raised the standard of evidence. Fragility that once remained hidden now surfaces early, the impact of survivorship bias became more difficult to overlook, and robustness matters more than backtest appeal. At the same time, software has evolved from fragmented tools into integrated systems where data, signals, portfolios, and risk are designed together. Quantitative investing has quietly changed character becoming process-driven rather than model-driven, with resilience taking precedence over elegance.

Data, Patterns, and the Shift Beyond Factors

“We don’t start with an economic theory. We start with the data.” - Jim Simons

While data availability expanded rapidly, progress came not from volume alone, but from how data was treated. Early quantitative strategies focused almost exclusively on prices and volumes. Modern systems emphasise pattern recognition, extracting signals from cleaned, normalised datasets while explicitly accounting for survivorship bias, corporate actions, and structural distortions.

This shift has been particularly important in India. Sector leadership rotates frequently, liquidity is uneven across market capitalisations, and index composition itself evolves over time. Quantitative frameworks that fail to account for these realities often decay quietly rather than fail dramatically.

At the same time, strategy development has moved beyond static factor labels. One of the earliest known factors, the value factor, was introduced by Benjamin Graham in Security Analysis (1934), embedding numerical discipline into investment thinking. Decades later, Eugene Fama and Kenneth French formalised factor-based investing through their three-factor model, while Narasimhan Jegadeesh and Sheridan Titman laid the foundations for momentum investing.

Over time, academics and practitioners discovered a wide array of additional factors, giving rise to what is often referred to as the “factor zoo”, spanning value, momentum, quality, growth, and technical indicators. While these academically supported factors remain important inputs, modern quantitative investing increasingly supplements them with alpha signals derived from machine learning techniques and non-traditional datasets. Rather than asking whether a factor “works”, contemporary frameworks focus on signal behaviour, strength, persistence, decay, and interaction across regimes. Backtesting: From Demonstration to Validation

Backtesting: From Demonstration to Validation

In India, quantitative investing began to evolve meaningfully only when technology narrowed the gap between theory and execution. Until the early 2010s, research was constrained by on-premise infrastructure, limited parallel processing, and high computing costs. Strategy development was selective backtests were narrow, histories were short, and stress-testing across market regimes was difficult.

As hardware costs fell and cloud adoption accelerated, these constraints eased. Broader datasets, longer backtests, and multi-factor frameworks became feasible alongside improvements in market infrastructure and data quality. Today, elastic cloud computing and large-scale parallel processing allow strategies to be tested across decades and regimes within hours. The limiting factor is no longer computation, but judgement identifying signals that remain robust beyond the backtest.

This shift has raised the standard of evidence. Fragility is exposed earlier, survivorship bias is harder to ignore, and resilience across cycles has become essential. At the same time, research tools have converged into integrated systems where data, signals, portfolios, and risk are designed together. Quantitative investing in India has quietly become process-driven rather than model-driven, with robustness taking precedence over elegance.

Machine Learning, New Data, and Modern Alpha

Advances in computing power have transformed both the scale and scope of quantitative investing. Techniques such as machine learning and natural language processing now allow investors to systematically analyse unstructured information—regulatory filings, earnings calls, and corporate disclosures—at a speed and depth that were previously impractical.

Large language models convert text into measurable signals, while cloud and GPU-based computing enable research and portfolio construction to be completed in hours rather than days. These capabilities generate stock-specific alpha signals that complement traditional factors, expanding the opportunity set without replacing proven frameworks.

As the number of signals has grown, so has the importance of how they are combined. Modern portfolio optimisers now account for interaction effects, regime shifts, and real-world constraints, while scaling efficiently across large investment universes. Importantly, increased technical sophistication has not reduced the role of human judgement; strong governance remains essential to ensure models remain intuitive, robust, and aligned with market reality.

Quantitative Investing as Long-Term Active Management

One of the most persistent misconceptions about quantitative investing is that it is synonymous with trading. In reality, quantitative methods are increasingly used to construct long-term, actively managed portfolios.

Active quant management does not imply frequent turnover. It implies continuous evaluation. Signals, correlations, and risks are monitored consistently, even when portfolio changes are incremental. The objective is not to predict market turning points, but to remain aligned with prevailing market structure while managing downside through rules rather than discretion.

Modern long-only quantitative frameworks, such as Dolat Quantum Leap, reflect this approach. Built as rules-based systems integrating pattern recognition, relative strength, and trend analytics, these strategies are designed to remain sector-agnostic and adaptable across market regimes. The emphasis is on consistency of process rather than conviction in forecasts.

Atomic Decisions, Not Grand Calls

Perhaps the most understated advancement in quantitative investing has been the move toward atomic-level granularity. Modern systems do not wait for quarterly reviews or dramatic signals. They assess information continuously and adjust exposure incrementally.

The graduation from Binary to Linear quantitative computing marks a fundamental change in how information is processed. Instead of treating signals as switches that reduce information into 0-or-1 outcomes, modern systems assess multiple factors in parallel and respond to their collective magnitude.

Signals are monitored for decay. Risk is recalibrated dynamically. Portfolios evolve quietly.

Over long horizons, this granularity compounds not through bold calls, but through restraint. For portfolio construction, it represents a shift away from episodic judgment toward continuous alignment.

“In quant investing, small decisions made consistently matter more than bold calls made occasionally.”

Infrastructure and Institutional Discipline

Quantitative investing today is as much about infrastructure as insight. Sophisticated strategies require high-performance computing, secure data pipelines, resilient execution systems, and strong governance frameworks. This is why quant investing has increasingly taken on an institutional character globally.

In India, this infrastructure build-out is still underway, but accelerating. Asset managers investing in technology, research platforms, and governance are better positioned to sustain performance across cycles. Competitive advantage increasingly lies not only in ideas, but in the ability to test, deploy, and supervise strategies consistently at scale.

India’s Opportunity Over the Next Decade

Globally, systematic investing has already crossed into the mainstream. In India, adoption remains earlier, but the direction of travel is clear. As data quality improves, institutional participation deepens, and market complexity increases, the case for disciplined, rules-based frameworks will only strengthen.

The next phase of quantitative investing will not be defined by novelty or model complexity alone. It will be defined by robustness, systems that integrate multiple signals, manage risk continuously, and adapt to changing regimes without sacrificing process integrity. Quantitative investing has come a long way from rules, ratios, and regression. Its most important contribution is not superior prediction, but better behaviour at scale.

The next decade is likely to mark the transition of quantitative investing in India from a niche capability to a foundational element of institutional portfolio construction.

Recent Blogs

SEBI’s GARUDA Framework: A Big Boost for India’s AIF Industry and GIFT City Ecosystem

Winners & Losers: Sectors to Watch in the Current Global Crisis

PMS Bazaar recently organized a webinar titled “Winners & Losers: Sectors to Watch in the Current Global Crisis,” which featured Mr. Arpit Shah, Co-Founder and Director, Care Portfolio Managers. This blog covers the important points shared in this insightful webinar.

Why Market Corrections Are the Best Time to Build Your Core Equity Portfolio

PMS Bazaar recently organized a webinar titled “Why Market Corrections Are the Best Time to Build Your Core Equity Portfolio,” which featured Mr. Amit Nigam, Deputy CIO, ASK Investment Managers. The webinar blog covers insights from Mr. Nigam, which includes explanation how recent stock market volatility in India creates opportunities for long-term investors. It highlights shifting from a fixed deposit mindset to equities, his blog covers the important points shared in this insightful webinar.

Why ETF-Only Portfolios Are the Most Tax-Efficient Way to Invest

How deferred taxation and lower LTCG rates compound into significantly higher post-tax wealth for long-term investors

6 out of 10 PMSes Beat Benchmarks In March Crash

Despite a fourth straight monthly sell-off, most PMSes fell less than benchmarks; a few even stayed in the green

Sapphire SIF: Long-Short Factor Model Driven by Quant Strategy

PMS Bazaar recently organized a webinar titled “Sapphire SIF: Long-Short Factor Model Driven by Quant Strategy,” which featured Mr. Satish Prabhu, Vice President and Head of Products and Content, Franklin Templeton Asset Management Private Limited. This blog covers the important points shared in this insightful webinar.

Why Invest in Start-Ups for Wealth Creation?

PMS Bazaar recently organized a webinar titled “Why Invest in Start-Ups for Wealth Creation?” which featured Mr. Vinit Rai, MD& CIO, Managing Director, JM Financial Equity. This blog covers the important points shared in this insightful webinar.

Why Investors Are Turning to Semi-Liquid Credit Funds?

PMS Bazaar recently organized a webinar titled “Why Investors Are Turning to Semi-Liquid Credit Funds?” which featured Mr. Dipen Ruparelia, Chief Business and Product Officer, Vivriti Asset Management. This blog covers the important points shared in this insightful webinar.