How deferred taxation and lower LTCG rates compound into significantly higher post-tax wealth for long-term investors

For most investors, the conversation around portfolio construction begins and ends with expected returns. Yet there is a second, equally decisive dimension that quietly determines long-term wealth outcomes: how much of those returns are retained after tax. In India's investment landscape, Exchange Traded Funds (ETFs) held directly in a personal Demat account offer a structural tax advantage that compounds dramatically over time. This article explains precisely how that advantage works, what it costs investors who ignore it, and why at Qode we have built our investment approach around this principle.

The Core Principle: ETFs Do Not Create Taxable Events Inside the Fund

One of the most important and widely misunderstood features of an ETF is how it handles internal portfolio activity. When an ETF rebalances to track its underlying index, whether it is replacing a constituent stock or adjusting weights, those internal transactions do not trigger a tax liability for the unit holder.

Tax is triggered only at one moment: when the investor sells their ETF units. Until that point, regardless of what is happening inside the fund, no capital gains are realised in the hands of the investor. The investor is fully in control of when the tax clock starts.

In an ETF, the unit holder pays tax only when they choose to sell. The fund's internal activity is invisible to the taxman.

This is fundamentally different from what happens in an active strategy, particularly one with high portfolio turnover, as we will illustrate with a detailed example below.

The Real Cost of High Churn: A Concrete Example

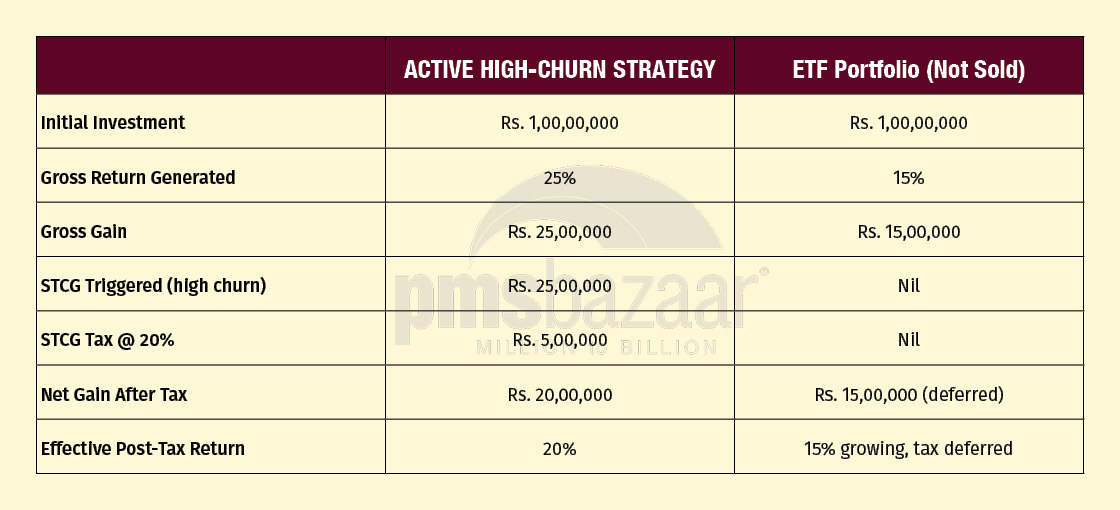

Consider a high-conviction active strategy that generates a gross return of 25% per annum. The fund manager achieves this through frequent repositioning, with a large portion of the portfolio held for less than 12 months. Under current Indian tax law, any gain on equity held for less than 12 months is classified as Short-Term Capital Gain (STCG) and taxed at 20%.

Here is what the numbers look like for an investor with an initial corpus of Rs. 1 crore:

The active strategy earns 25% but the investor keeps only 20%. That 5% is not lost to poor performance. It is lost entirely to tax. The fund manager delivered what they promised. The tax structure consumed the difference.

Now consider the ETF investor. Their gross return is 15%, which appears lower. But because they have not sold their units, no tax event has occurred. Their full Rs. 15 lakh in gains continues to compound. The deferred tax is in effect an interest-free loan from the government that the investor uses to generate further returns.

A 25% gross return taxed at 20% STCG becomes a 20% net return. A 15% ETF return with zero current-year tax remains 15% compounding in full. Over time, the ETF's compounding base is larger.

The Second Benefit: LTCG at 12.5% vs. STCG at 20%

Tax deferral is only the first advantage. The second is equally powerful: when an ETF investor does eventually sell, they pay Long-Term Capital Gains tax at 12.5%, not the 20% STCG rate that active strategies trigger annually on churned positions.

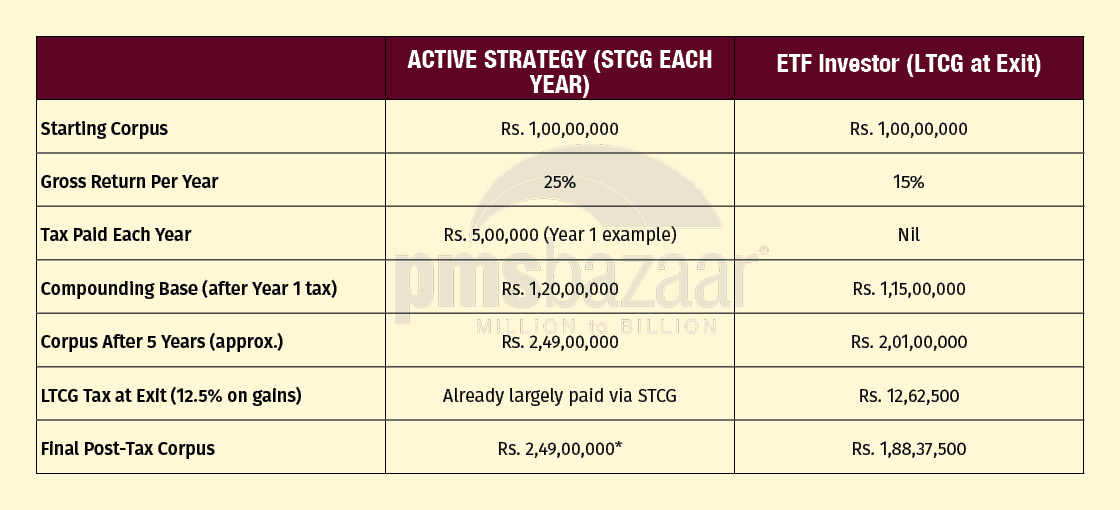

Let us extend the illustration. Assume both investors hold for five years before the ETF investor exits:

*The active strategy corpus is net of tax paid each year. However, this illustration uses a uniform 25% return assumption. Real-world active returns are variable and the STCG drag compounds negatively in down years as well.

In this specific comparison, the active strategy's gross return advantage of 10 percentage points does outperform. But the key takeaway is not which wins in this single example. It is the structural principle: every percentage point that the active strategy is taxed at 20% annually rather than 12.5% at exit represents a permanent drag that cannot be recovered. As the return differential narrows, the ETF's tax structure becomes increasingly decisive.

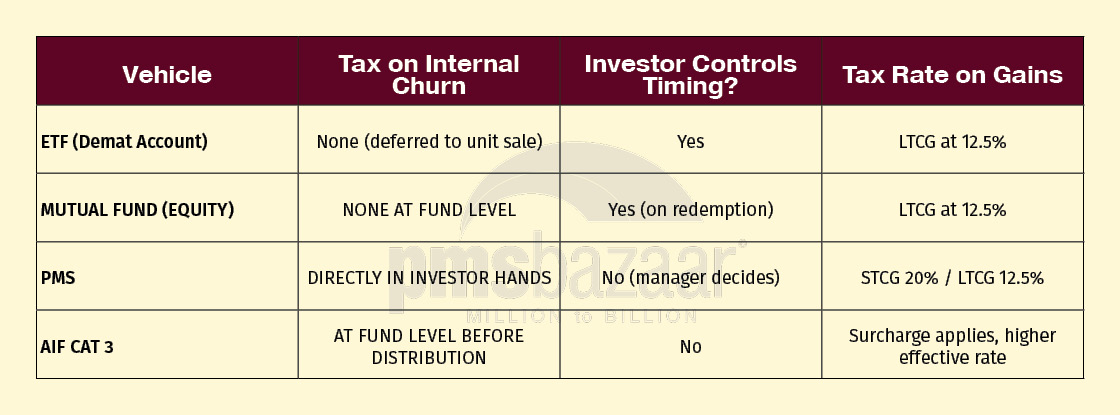

PMS and AIF Cat 3 Do Not Offer This Tax Advantage

It is important to address a common misconception among HNI investors. Portfolio Management Services (PMS) and Alternative Investment Funds Category 3 (AIF Cat 3) are often perceived as sophisticated, institutionally structured products. They are. But neither structure shields the investor from direct pass-through of tax liabilities in the same way that ETFs do.

In a PMS, the portfolio manager trades in securities held directly in the investor's Demat account. Every time the manager buys and sells a position, the resulting capital gain or loss is recognised in the investor's hands for that financial year. A PMS with 70% annual churn is effectively generating STCG for the investor on 70% of the portfolio's gains, every year, whether the investor asked for it or not.

In an AIF Cat 3, the structure is a trust or a company, and gains are taxed at the fund level before distribution. While this creates a different mechanism, it does not provide the investor with the benefit of deferral that an ETF held in a personal Demat account delivers.

The comparison is direct:

PMS and AIF Cat 3, despite their sophistication, do not give investors the structural tax deferral benefit that ETFs and direct mutual funds provide. This is a meaningful and often overlooked distinction.

Why Qode Takes Exposure to Strategies Through ETFs

At Qode, we have studied this dynamic closely and built our investment philosophy around it. We believe that the vehicle through which a strategy is accessed is as important as the strategy itself. A well-designed strategy delivered in a tax-inefficient wrapper will consistently underperform the same strategy accessed through a tax-efficient one.

This is why we take exposure to our strategies through ETFs. Rather than running high-churn active portfolios that generate annual STCG for our investors, we construct factor-based, rules-driven strategies and access them via ETF structures. The result is that our investors benefit from three compounding advantages simultaneously:

- Tax deferral: Gains compound without being reduced by annual STCG. The investor's full capital base keeps growing.

- Lower tax rate at exit: When investors do eventually sell, they pay LTCG at 12.5% rather than STCG at 20%, which represents a 37.5% reduction in the tax rate on those gains.

- Lower costs: ETF expense ratios in India typically range from 0.05% to 0.30% per annum, a fraction of what active strategies charge. Over 15 to 20 years, the cost differential compounds into a significant wealth advantage.

What ultimately matters to every investor is not the gross return on the factsheet. It is the post-tax, post-cost return that lands in their account. By structuring our strategies through ETFs, Qode ensures that a higher proportion of every rupee of return generated is retained by our investors, not surrendered to tax on a schedule they never chose.

Key Takeaways

FOR INVESTORS TO REMEMBER

- ETFs do not trigger tax on internal portfolio activity. Tax is paid only when you, the investor, choose to sell your units.

- A high-churn strategy generating 25% gross becomes 20% net after STCG of 20%. That 5% alpha is consumed entirely by tax, not by fees, not by underperformance.

- Deferring tax through ETFs means your full corpus continues to compound. The deferred tax functions as an interest-free loan that accelerates wealth creation.

- When you do eventually exit an ETF held for more than 12 months, your gains are taxed at LTCG of 12.5%, not STCG of 20%, a rate that is 37.5% lower.

- PMS and AIF Cat 3 do not provide this structural tax shield. In a PMS, the manager's trades create your tax liability. In AIF Cat 3, the fund pays tax before distributing returns to you.

- The vehicle matters as much as the strategy. A good strategy accessed through a tax-inefficient structure will consistently deliver lower post-tax returns than a comparably good strategy accessed through ETFs.

- At Qode, we access our strategies through ETFs specifically to ensure our investors receive the highest possible post-tax returns. This is not incidental to our philosophy. It is central to it.

Disclaimer: This article is for educational and informational purposes only and does not constitute investment advice. Tax rates mentioned are as per applicable Indian income tax provisions and are subject to change. Readers are advised to consult their financial and tax advisors before making any investment decisions.

Recent Blogs

Early-Stage Access to India's Manufacturing Growth Story

PMS Bazaar recently organized a webinar titled “Early-Stage Access to India's Manufacturing Growth Story,” which featured Mr. Vignesh Shankar, Founder & Managing Partner, a99 VC. This blog covers the important points shared in this insightful webinar.

May sees selective alpha as PMSes navigate market consolidation

Despite a subdued market environment, PMS strategies continued to deliver positive returns. Leadership remained concentrated in Thematic, Small Cap and Small & Midcap categories, underscoring the value of active management and focused portfolio positioning.

SEBI’s Accredited Investor Certificate: Exclusive Access to AIFs, PMS, SIFs & Private Markets

PMS Bazaar recently organized a webinar titled “SEBI’s Accredited Investor Certificate: Exclusive Access to AIFs, PMS, SIFs & Private Markets,” which featured Mr. Rajesh Kumar S, Head of Business, NSDL Database Management Limited. This blog covers the important points shared in this insightful webinar.

April rebound lifts PMS strategies, but small-cap tilt drives leaders

A broad market recovery helped managers beat large-cap indices, though alpha against wider benchmarks remained more selective and category-dependent

SEBI’s GARUDA Framework: A Big Boost for India’s AIF Industry and GIFT City Ecosystem

India’s Alternative Investment Fund (AIF) industry has evolved rapidly over the last few years. Investors today are increasingly moving beyond traditional investment products such as mutual funds and fixed deposits in search of differentiated opportunities across Private Equity, Venture Capital, Private Credit, Real Estate, infrastructure, and Category III long-short strategies.

Winners & Losers: Sectors to Watch in the Current Global Crisis

PMS Bazaar recently organized a webinar titled “Winners & Losers: Sectors to Watch in the Current Global Crisis,” which featured Mr. Arpit Shah, Co-Founder and Director, Care Portfolio Managers. This blog covers the important points shared in this insightful webinar.

Why Market Corrections Are the Best Time to Build Your Core Equity Portfolio

PMS Bazaar recently organized a webinar titled “Why Market Corrections Are the Best Time to Build Your Core Equity Portfolio,” which featured Mr. Amit Nigam, Deputy CIO, ASK Investment Managers. The webinar blog covers insights from Mr. Nigam, which includes explanation how recent stock market volatility in India creates opportunities for long-term investors. It highlights shifting from a fixed deposit mindset to equities, his blog covers the important points shared in this insightful webinar.

6 out of 10 PMSes Beat Benchmarks In March Crash

Despite a fourth straight monthly sell-off, most PMSes fell less than benchmarks; a few even stayed in the green