Despite a fourth straight monthly sell-off, most PMSes fell less than benchmarks; a few even stayed in the green

Amid the US/Israel-Iran war, March 2026 was one of the toughest months in recent years for PMS investors, with the market extending its decline for a fourth straight month. Foreign institutional investors continued to sell aggressively even as domestic inflows touched record highs. Weakness was broad-based: 46 of the 50 Nifty stocks ended lower during the month, while PSU Banks fell 20 per cent, Real Estate 17 per cent, Private Banks and Automobiles 16 per cent each, and Financials 14 per cent.

Against this backdrop, the PMSBazaar study tracked 518 schemes, including 461 equity, 18 debt, 36 multi-asset and 3 hybrid schemes. Equity PMSes, on average, fell 10.65 per cent in March, slightly less than the 11.3 per cent decline in the Nifty 50 TRI and the 11.37 per cent fall in the S&P BSE 500 TRI. Importantly, a majority of PMSes still managed to hold up better than the benchmarks. As many as 270 equity schemes, or 59 per cent, outperformed the Nifty 50 TRI, while 272 schemes, again 59 per cent, beat the S&P BSE 500 TRI.

The range of returns, however, remained unusually wide. The best-performing equity PMS, Qode Advisors’ Qode Growth Fund, gained 1.34 per cent during the month, while the bottom of the table declined 22.08 per cent. That sharp dispersion highlights how significant manager selection was in March. Even in a falling market, a handful of strategies were able to protect capital far better than peers.

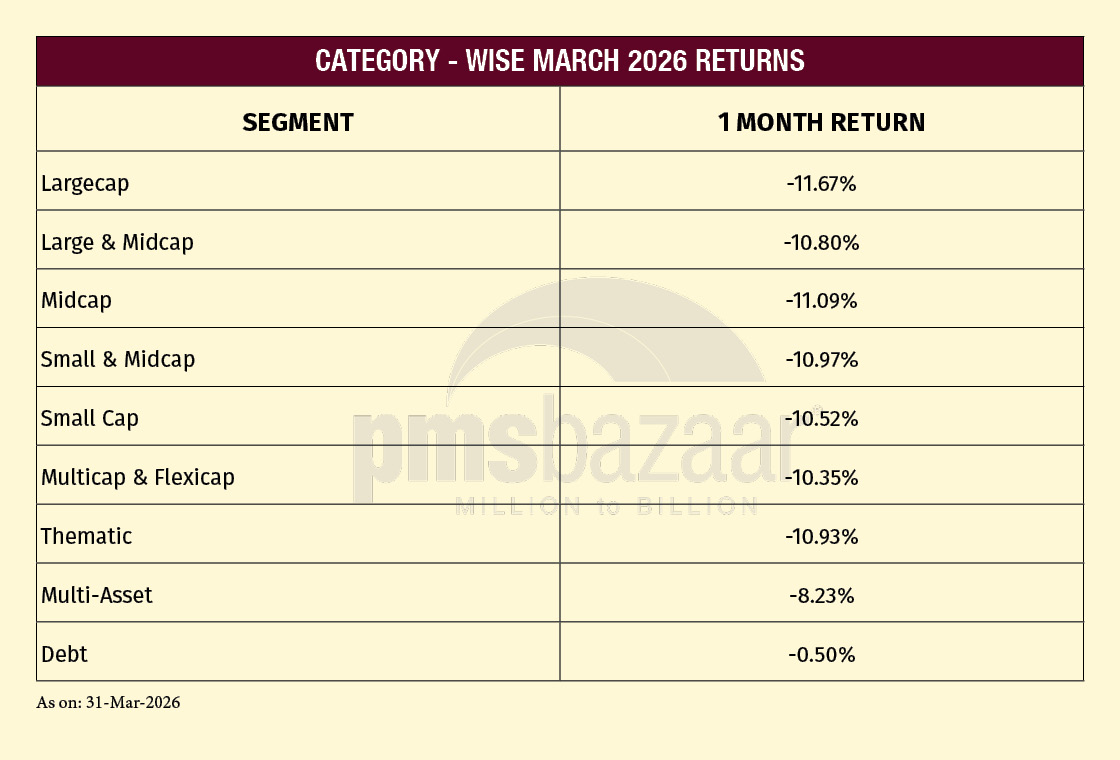

At the category level, diversified equity strategies proved relatively resilient. Multicap & Flexicap PMSes saw the smallest average decline at 10.35 per cent, followed by Small Cap at 10.52 per cent and Large & Midcap at 10.80 per cent. Large-cap PMSes were the weakest, slipping 11.67 per cent on average. Multi-asset strategies limited losses better at 8.23 per cent, while debt PMSes were down only 0.5 per cent.

Let us take a detailed look at PMS performance through the month.

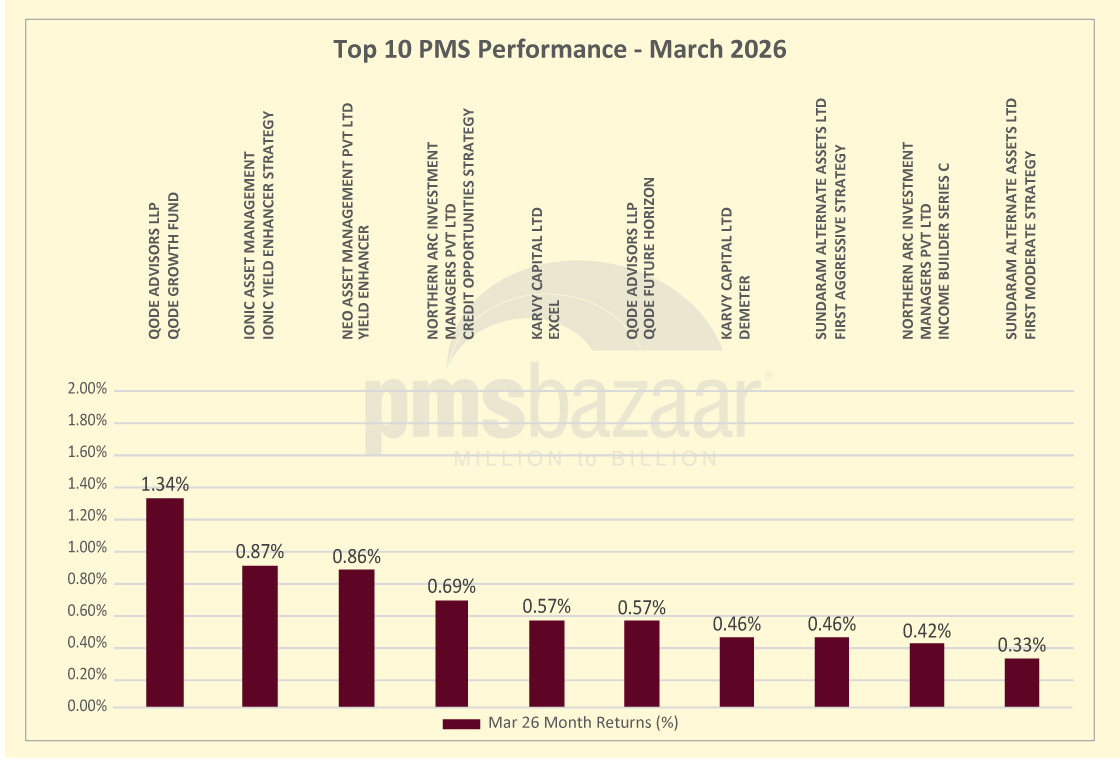

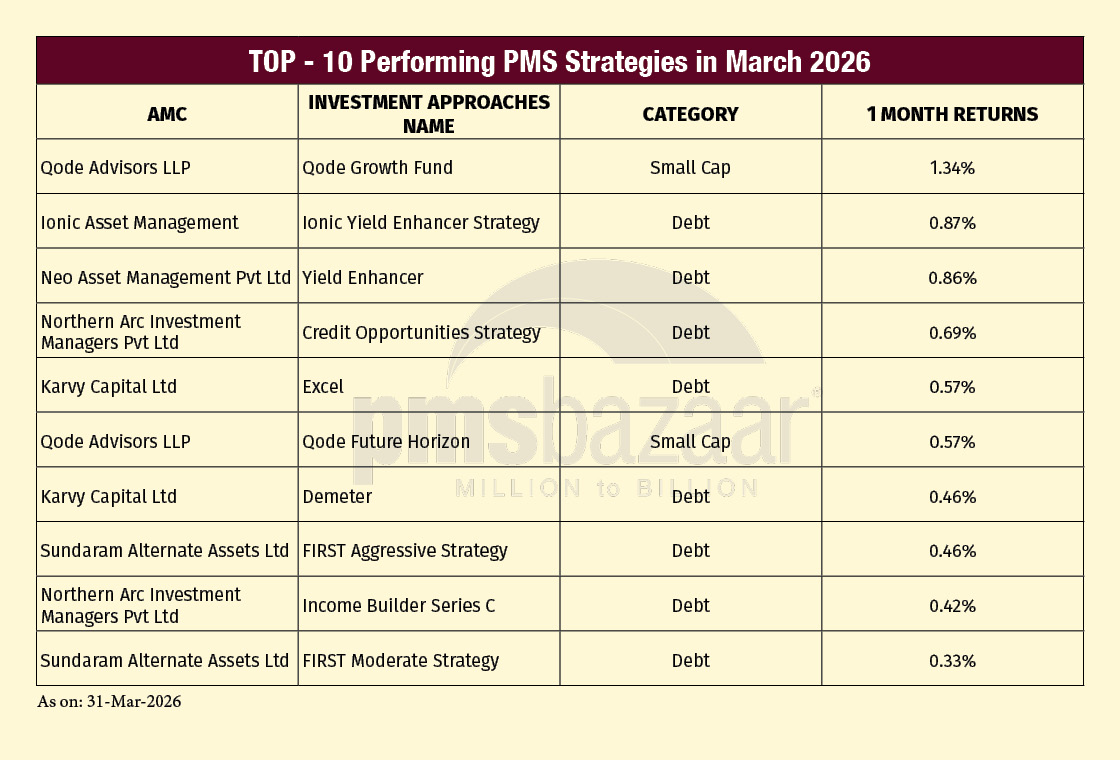

Top-10 performers

March’s overall top-10 PMS list, across all asset classes, was dominated by debt strategies as fixed-income portfolios proved far more resilient than equities during the market sell-off. Of the 10 best-performing PMSes in March, seven were debt schemes. Ionic Asset Management’s Ionic Yield Enhancer Strategy ranked second overall with a 0.87 per cent return, followed closely by Neo Asset Management’s Yield Enhancer at 0.86 per cent and Northern Arc’s Credit Opportunities Strategy at 0.69 per cent. Karvy Capital’s Excel and Demeter, Sundaram Alternate Assets’ FIRST Aggressive and FIRST Moderate strategies, and Northern Arc’s Income Builder Series C also featured in the top 10. The only equity PMSes to post gains were Qode Advisors’ Qode Growth Fund and Qode Future Horizon, while Value Prolific’s Conserve C ended flat. The composition of the list underlines how sharply March favoured capital preservation over return-seeking. With equity markets down more than 11 per cent, debt PMSes emerged as the month’s clear relative winners.

If you look at just the top-10 equity PMSes, it reveals quite a lot.

March 2026’s top-performing PMS list looks very different from the usual pattern. In a month when the average equity PMS fell 10.65 per cent and the broader market corrected for a fourth straight month, simply preserving capital became a form of outperformance. The top-10 list was therefore defined less by aggressive upside capture and more by limiting damage far better than peers and benchmarks.

Qode Advisors emerged as the clear standout. Its Qode Growth Fund was the only equity PMS in the study to end the month in positive territory, gaining 1.34 per cent despite the Nifty 50 TRI and S&P BSE 500 TRI falling more than 11 per cent. Qode Future Horizon followed with a 0.57 per cent gain. Qode also featured twice more in the top 10 through Qode Tactical Fund and Qode All Weather, underlining the consistency of its investment approach across strategies.

The broader composition of the list is equally revealing. Small-cap strategies led the rankings, with both the top two performers belonging to that category. Yet the remainder of the list was dominated by multi-cap and flexicap offerings such as Investvalue Capital’s India Winners Portfolio, Envision Capital’s New Frontiers and Capital 8 Infinity Fund.

What stands out is that even the tenth-best equity PMS fell 4.16 per cent. In most months, that would not qualify as strong performance. But March was not a normal month. With benchmark indices down more than 11 per cent and sectoral losses reaching as much as 20 per cent in PSU banks, the month rewarded defensiveness, cash management and disciplined stock selection far more than outright risk-taking.

Category overview: How March 2026 was

Category-level performance in March 2026 shows that no part of the equity market was spared from the sharp correction. Every PMS equity category ended in the red, with average losses ranging from 10.35 per cent to 11.67 per cent. Even so, the degree of decline varied meaningfully across segments, suggesting that portfolio flexibility and diversification still helped cushion the fall.

Multicap & Flexicap strategies proved the most resilient among equity PMS categories, with an average decline of 10.35 per cent. Small Cap schemes followed at 10.52 per cent, while Large & Midcap strategies fell 10.80 per cent. These categories held up somewhat better than the overall equity PMS average decline of 10.65 per cent and also performed slightly better than the Nifty 50 TRI and S&P BSE 500 TRI, both of which fell more than 11 per cent.

Midcap, Small & Midcap and Thematic strategies clustered in a narrower range, with average declines of 11.09 per cent, 10.97 per cent and 10.93 per cent respectively. Thematic PMSes did not suffer as badly as might have been expected in a month marked by sharp sectoral weakness, but their concentrated nature still left little room for error.

Largecap PMSes were the weakest-performing equity category, falling 11.67 per cent on average. That is notable because large-cap strategies are often expected to provide relative stability in difficult markets. But March’s sell-off was led by heavyweight sectors such as banks, financials and automobiles, which hurt benchmark-oriented portfolios more sharply.

Outside equities, defensive categories clearly stood apart. Multi-asset PMSes limited losses to 8.23 per cent, benefiting from exposure beyond equities, while debt PMSes were down only 0.5 per cent. The broader message from March is that diversification mattered more than style. Flexible and asset-diversified strategies were better able to protect capital than narrowly benchmark-linked portfolios.

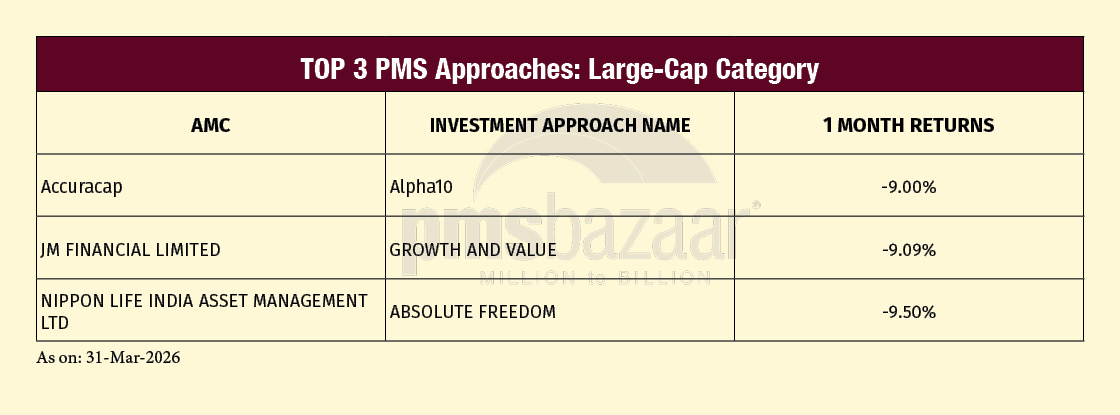

Large-cap PMSes struggle as benchmark-heavy sectors drag returns

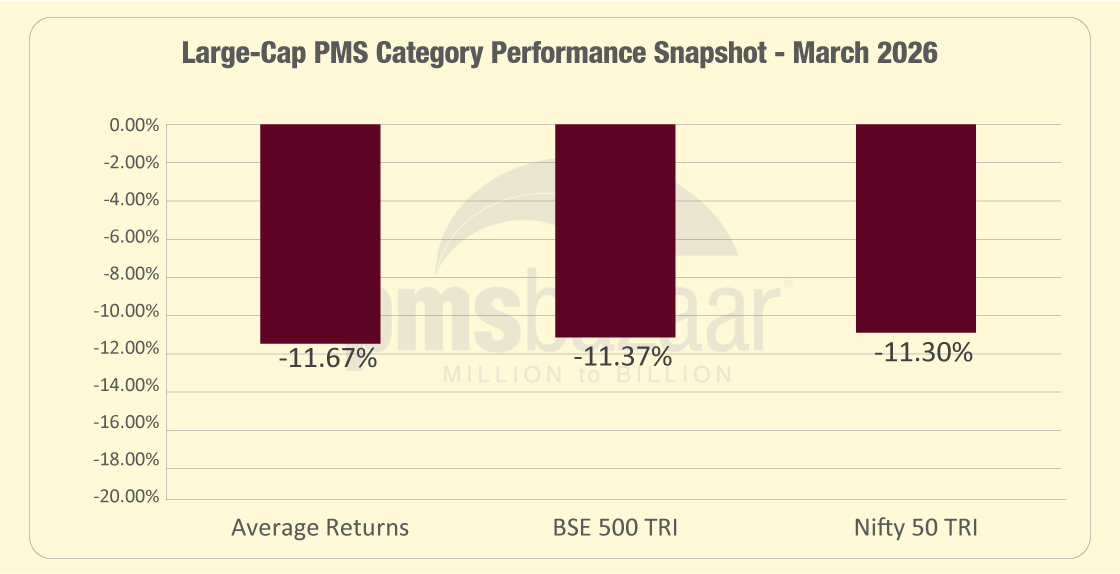

Large-cap PMSes were the weakest-performing equity category in March 2026. Across 33 schemes, the average decline stood at 11.67 per cent, marginally worse than both the S&P BSE 500 TRI’s 11.37 per cent fall and the Nifty 50 TRI’s 11.30 per cent decline. Only 11 schemes managed to outperform each of the two benchmarks, indicating that the category struggled to provide the downside protection investors typically expect from large-cap strategies.

That underperformance is not entirely surprising when viewed against the market backdrop. March’s sell-off was led by large benchmark-heavy sectors such as PSU banks, private banks, financials and automobiles. Since most large-cap PMSes tend to remain relatively close to the index in sector composition, they had limited scope to escape the sharp correction.

Even within this difficult environment, a few strategies managed to hold up better than peers.. Accuracap’s Alpha10 followed with a 9 per cent decline, while JM Financial’s Growth and Value fell 9.09 per cent. At third, Nippon Life India Asset’s Absolute Freedom fell -9.50 percent. That is a notable result in a month when the category average decline exceeded 11 per cent.

That suggests manager selection still mattered, but less so than in broader-market categories where portfolio flexibility offered greater room to avoid the worst-hit sectors.

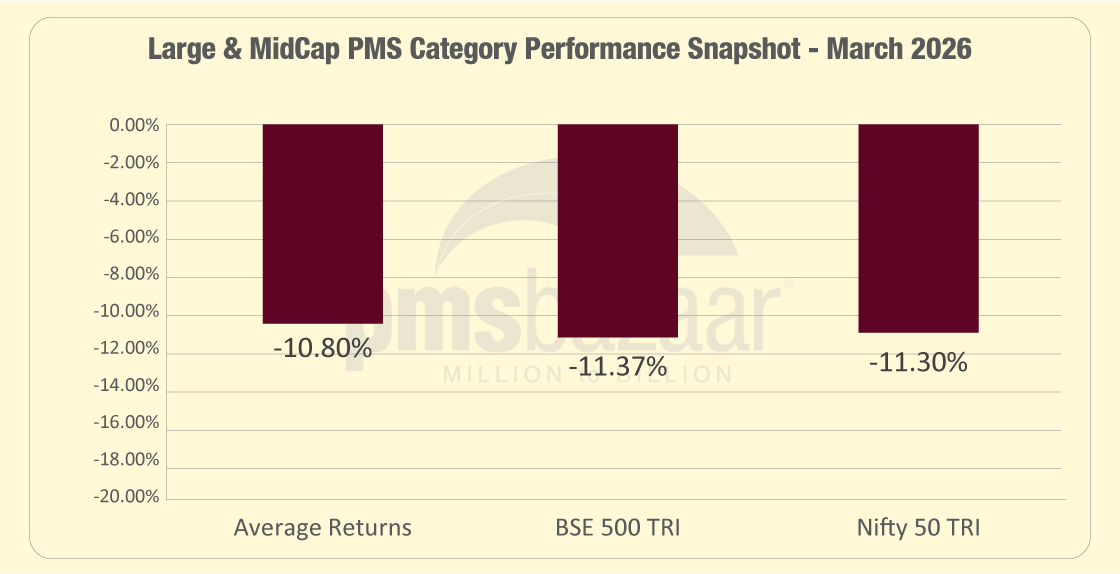

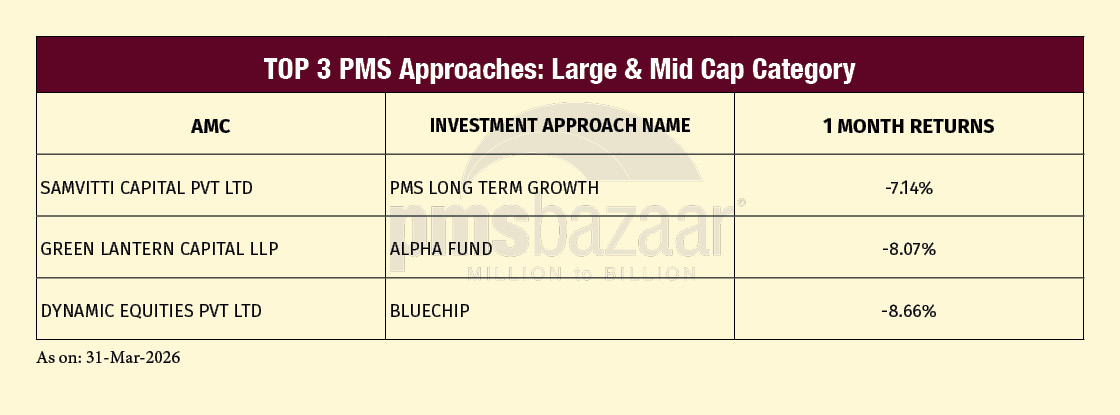

Large & Midcap PMSes try to prove resilience in March sell-off

Large & Midcap PMSes were among the better-performing equity categories in March 2026. Across 24 schemes, the average decline stood at 10.80 per cent, lower than both the S&P BSE 500 TRI’s 11.37 per cent fall and the Nifty 50 TRI’s 11.30 per cent decline. Fifteen schemes outperformed each of the two benchmarks, suggesting that the category’s blend of large-cap stability and selective mid-cap exposure helped cushion the market correction.

That relative resilience is notable because March was particularly punishing for large benchmark-heavy sectors such as banks, financials and automobiles. Large & Midcap PMSes appear to have benefited from being less tied to the index than pure large-cap strategies, while still avoiding some of the sharper drawdowns seen in more aggressive market segments.

Samvitti Capital’s PMS Long Term Growth was the best-performing strategy in the category, declining 7.14 per cent. In a month when the category average was down nearly 11 per cent, that represents a meaningful degree of downside protection. Green Lantern Capital’s Alpha Fund followed with an 8.07 per cent fall, while Dynamic Equities’ Bluechip strategy declined 8.66 per cent.

That indicates manager selection mattered more in this category than in large-cap PMSes, with the additional flexibility across market-cap buckets giving managers more room to defend capital.

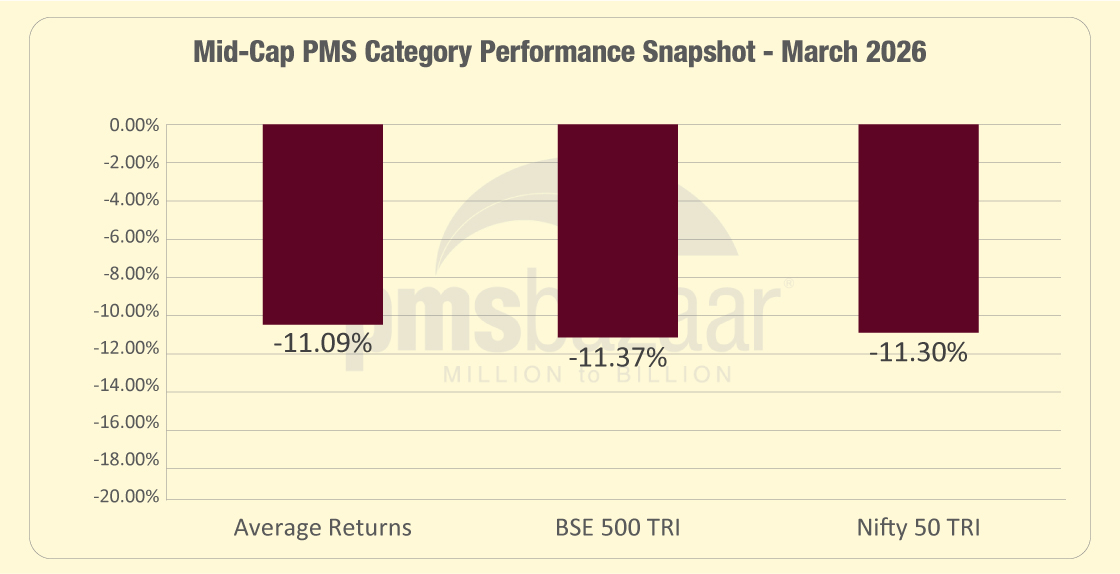

Mid-cap PMSes hold up better than benchmarks, but losses remain steep

Mid-cap PMSes fared slightly better than the broader market in March 2026, though the category still suffered a sharp correction. Across 23 schemes, the average decline was 11.09 per cent, marginally lower than the S&P BSE 500 TRI’s 11.37 per cent fall and the Nifty 50 TRI’s 11.30 per cent decline. Twelve schemes managed to outperform each benchmark, indicating that manager selection remained important even in a difficult month.

The category’s relative resilience is somewhat notable because mid-cap stocks are often expected to fall more sharply in risk-off periods. Instead, March’s sell-off was led by large-cap financials, banks and automobiles, which narrowed the gap between mid-cap and large-cap performance. Mid-cap managers with lower exposure to those sectors and a more selective stock approach were therefore able to preserve capital somewhat better.

Master Portfolio Services’ Master Trust India Growth Strategy was the best-performing mid-cap PMS, falling 8.70 per cent. Dynamic Equities’ Midcap Mavens was close behind at 8.71 per cent, while Nippon Life India AMC’s Emerging India declined 9.10 per cent.

That suggests the category offered some scope for downside protection, but not enough to fully escape the broad-based correction. Compared with Large & Midcap and Multicap PMSes, the room for differentiation within mid-cap portfolios appears to have been narrower.

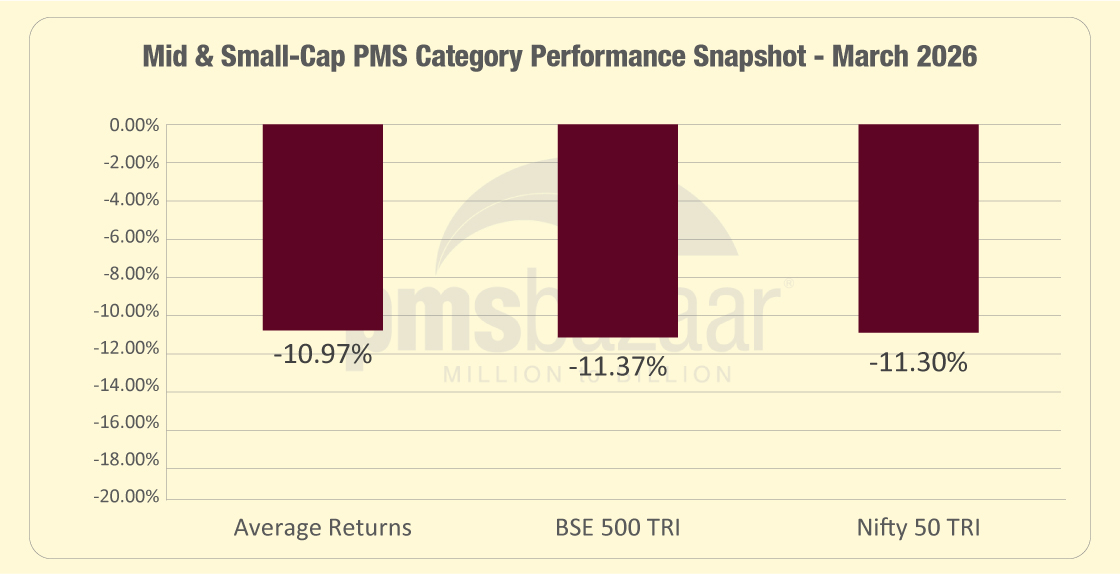

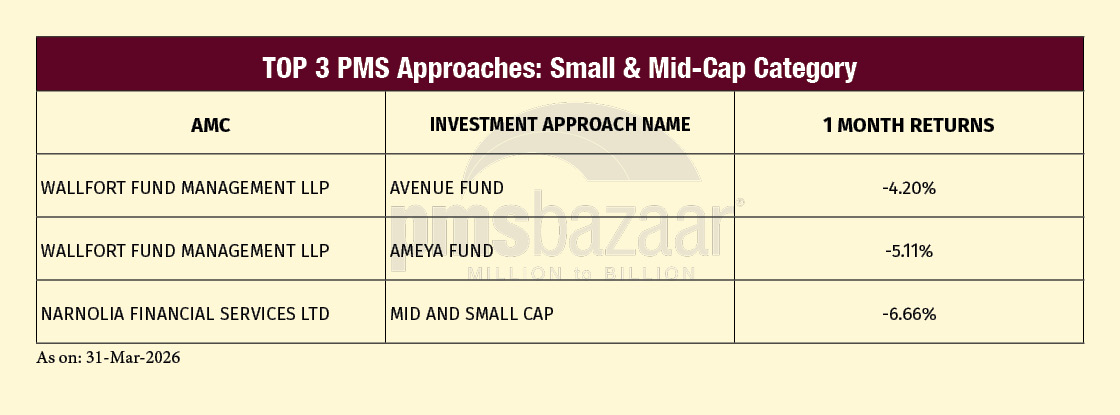

Mid & Small-cap PMSes show the widest gap between winners and losers

Mid & Small-cap PMSes delivered a better-than-benchmark performance in March 2026, though the category remained deep in negative territory. Across 58 schemes, the average decline stood at 10.97 per cent, lower than both the S&P BSE 500 TRI’s 11.37 per cent fall and the Nifty 50 TRI’s 11.30 per cent decline. Thirty-three schemes beat the BSE 500 TRI, while 32 outperformed the Nifty 50 TRI, indicating that more than half the category managed to preserve capital better than the benchmarks.

What stands out most in this category is the unusually wide dispersion in returns. Wallfort Fund Management’s Avenue Fund was the best-performing Mid & Small-cap PMS, declining just 4.20 per cent. Its Ameya Fund followed at 5.11 per cent. Both losses were far smaller than the category average and less than half the benchmark decline, suggesting that a few managers were able to position portfolios defensively even within the riskier end of the market.

Narnolia Financial Services’ Mid and Small Cap strategy with declines 6.66 per cent. Several of these portfolios appear to have benefited either from selective sector positioning or from holding higher cash levels during the correction.

That suggests this segment offered greater scope for managers to add value than large-cap or mid-cap PMSes, but also carried a higher penalty for getting the positioning wrong. March therefore reinforced a familiar pattern: in Mid & Small-cap PMSes, manager selection matters far more than category exposure alone.

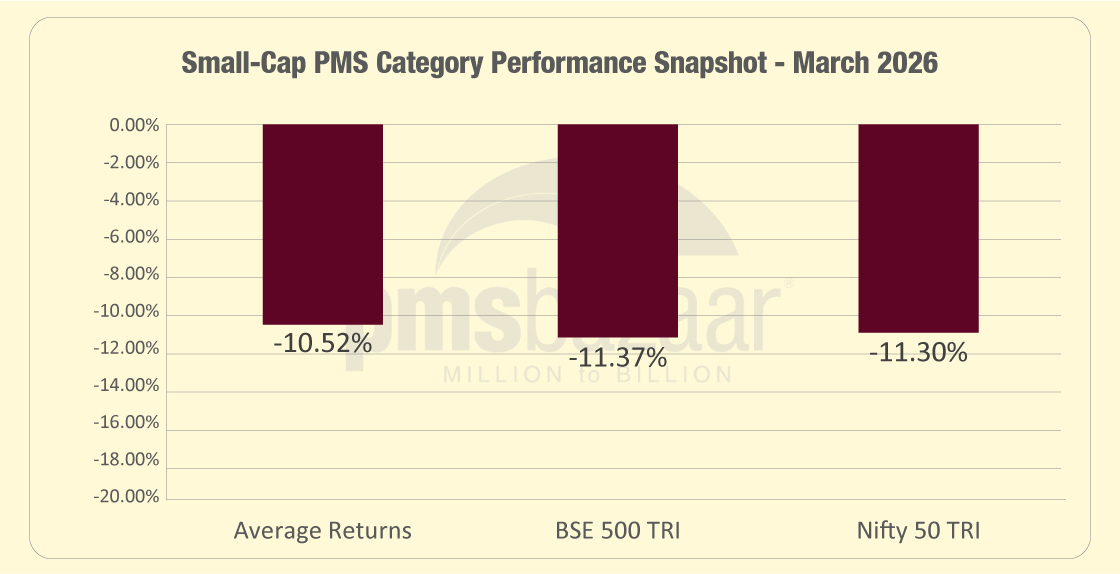

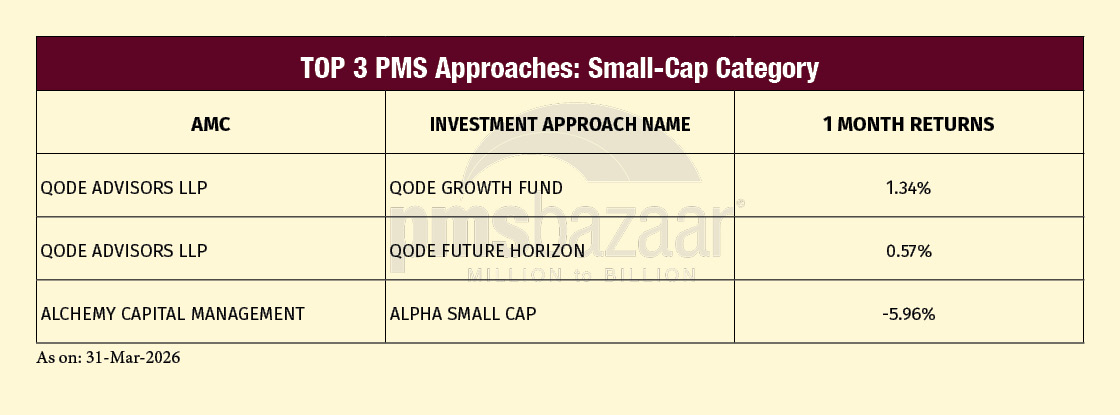

Small-cap PMSes deliver the sharpest upside protection in a falling market

Small-cap PMSes were among the most resilient equity categories in March 2026. Across 27 schemes, the average decline stood at 10.52 per cent, better than both the S&P BSE 500 TRI’s 11.37 per cent fall and the Nifty 50 TRI’s 11.30 per cent decline. Fourteen schemes outperformed the BSE 500 TRI, while 13 beat the Nifty 50 TRI, showing that roughly half the category managed to hold up better than the benchmarks despite the broad market rout.

What makes this category stand out is not just the average performance, but the top-end protection delivered by a few managers. Qode Advisors’ Qode Growth Fund was the best-performing equity PMS across the entire PMSBazaar study, gaining 1.34 per cent in a month when the market fell more than 11 per cent. Qode Future Horizon also stayed in positive territory with a 0.57 per cent gain. That two small-cap strategies generated positive returns in such a month is striking and points to highly differentiated stock selection and portfolio construction.

Beyond the top two, performance weakened but still remained meaningfully better than the category average. Alchemy Capital’s Alpha Small Cap fell 5.96 per cent,

That suggests small-cap PMSes offered some of the highest scope for manager-led outperformance in March, but also remained vulnerable for portfolios that were less selective. In a falling market, this category once again showed that manager selection can matter more than market-cap label alone.

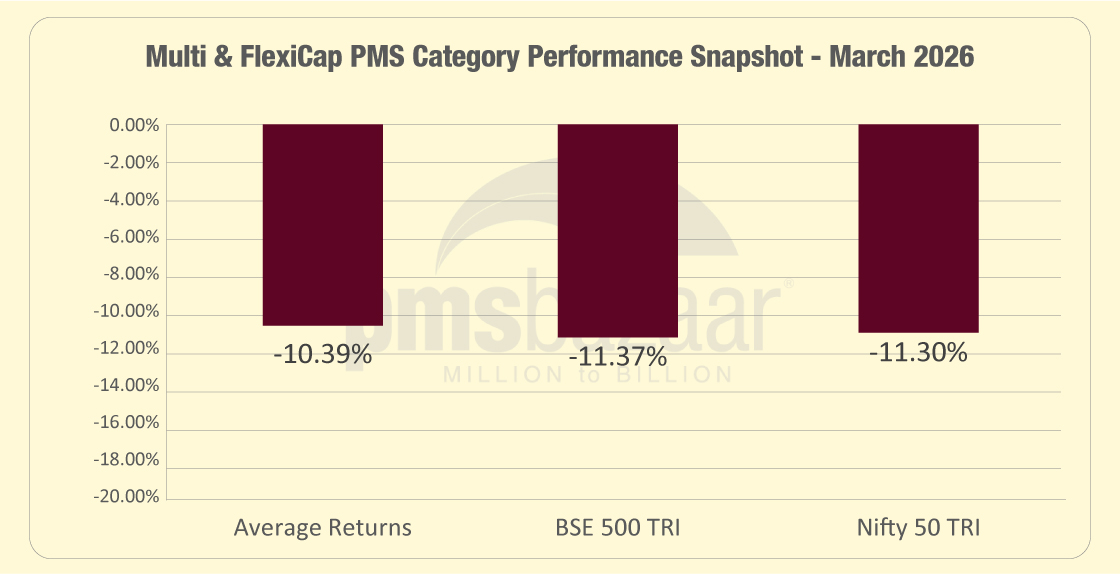

Multi & Flexicap PMSes emerge as the steadiest equity category in March

Multi & Flexicap PMSes were the best-performing equity category in March 2026. Across 268 schemes, the average decline stood at 10.39 per cent, the shallowest among all equity PMS segments and comfortably better than both the S&P BSE 500 TRI’s 11.37 per cent fall and the Nifty 50 TRI’s 11.30 per cent decline. The breadth of outperformance was also strong: 170 schemes beat the BSE 500 TRI, while 168 outperformed the Nifty 50 TRI.

That combination of scale and resilience makes this category particularly important. As the largest PMS segment by number of schemes, Multi & Flexicap performance offers the clearest picture of how active equity managers handled March’s fourth straight monthly market decline. The results suggest that flexibility across market-cap buckets and styles helped many managers cushion the sell-off better than more rigid mandates.

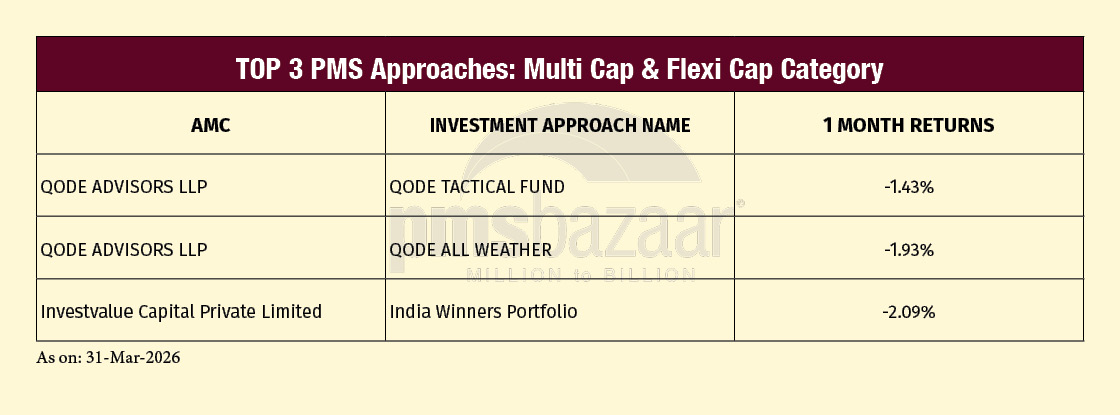

The top performers in the category underline that point.,. Qode Advisors featured twice again through Qode Tactical Fund and Qode All Weather, which fell only 1.43 per cent and 1.93 per cent respectively. Followed by Investvalue Capital India winners portfolio with -2.09 per cent an exceptionally strong showing in a month when equity benchmarks fell more than 11 per cent

In March, simply being diversified was not enough; the strongest outcomes came from managers who used that flexibility well. Among all equity PMS buckets, Multi & Flexicap strategies offered the clearest evidence that portfolio construction and stock selection could still materially soften the blow of a market-wide correction.

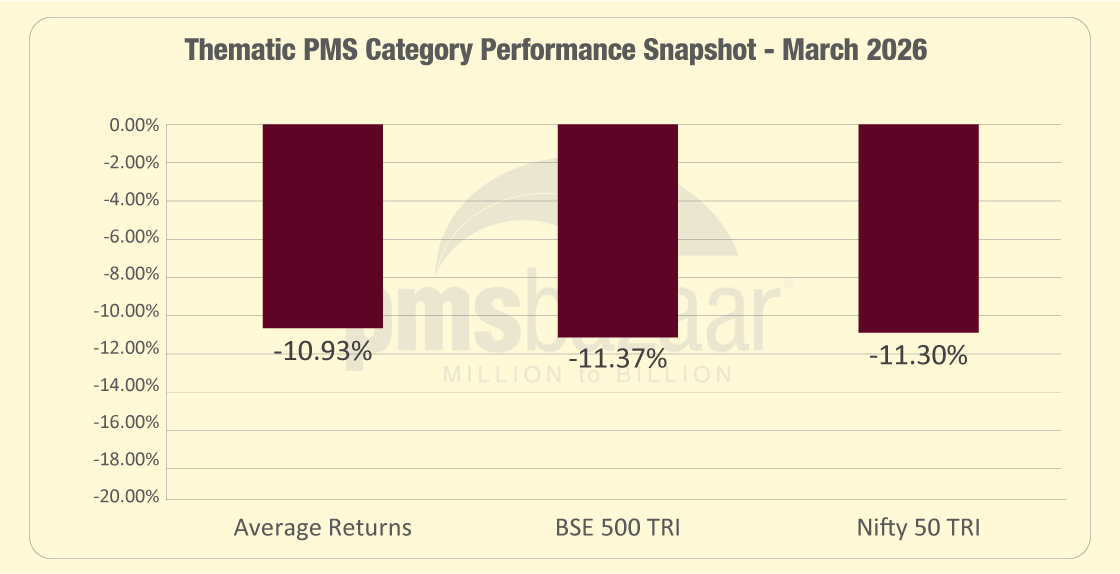

Thematic PMSes stay competitive, but concentration remains a double-edged sword

Thematic PMSes held up slightly better than the broader market in March 2026, though the category still posted a steep average decline of 10.93 per cent. Across 21 schemes, 13 outperformed the S&P BSE 500 TRI and an equal number beat the Nifty 50 TRI, suggesting that a majority of managers were able to protect capital somewhat better than the benchmarks despite the difficult market backdrop.

That result is more balanced than one might expect in a month marked by widespread sectoral weakness. March saw heavy damage in banks, financials, automobiles and real estate, but thematic PMSes were not uniformly hit because outcomes depended heavily on where managers were positioned. In a concentrated category, the right theme can still cushion returns, while the wrong one can amplify losses.

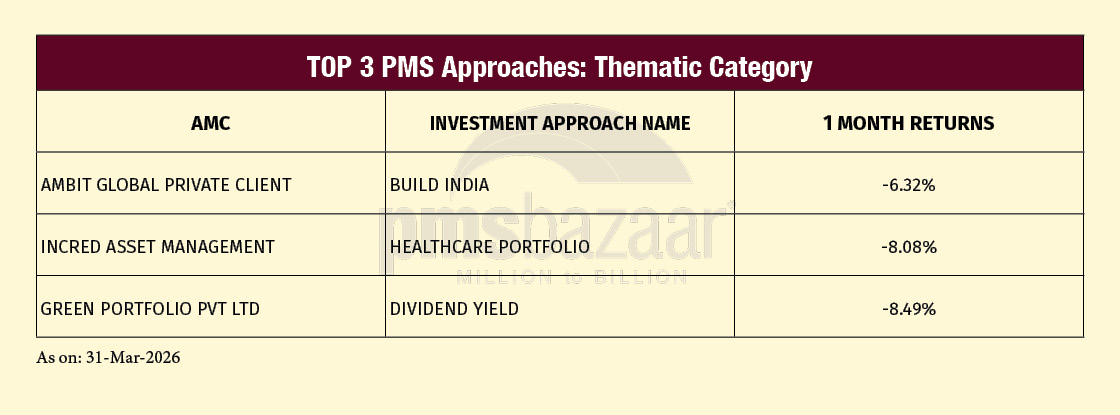

Ambit Global Private Client’s Build India was the best-performing thematic PMS, declining 6.32 per cent. InCred Asset Management’s Healthcare Portfolio followed with an 8.08 per cent fall, while Green Portfolio’s Dividend Yield strategy was down 8.49 per cent. That underlines the core feature of thematic PMS investing: it can produce differentiated outcomes, but it offers less margin for error than broader diversified mandates. In March, thematic strategies neither collapsed nor excelled as a group; instead, they once again proved highly dependent on the relevance of the chosen theme.

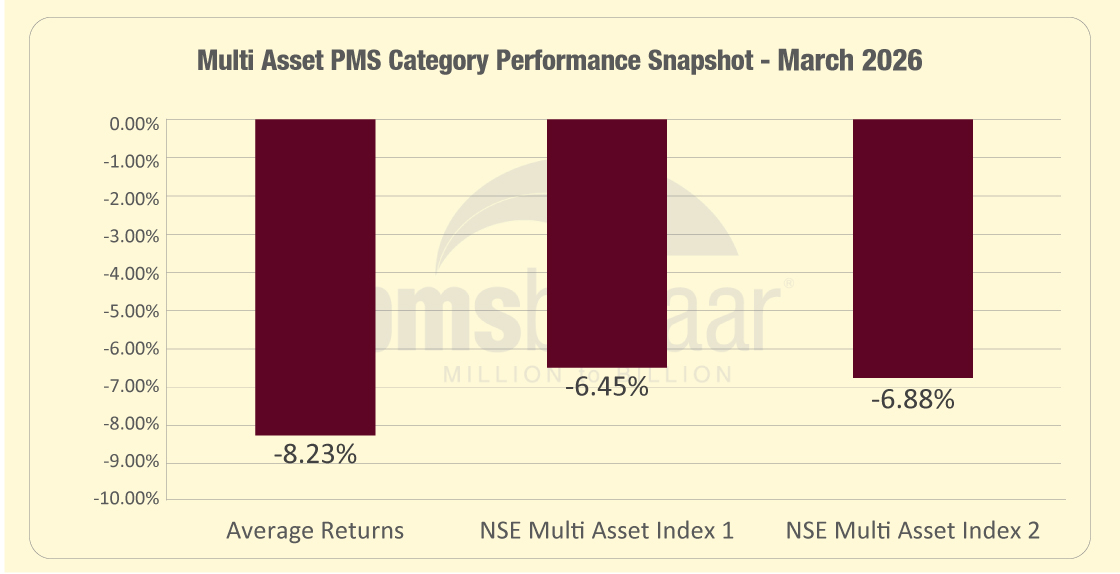

Multi-asset PMSes limit damage, but most still trail their own benchmarks

Multi-asset PMSes were clearly more resilient than equity PMSes in March 2026, but the category still underperformed its own reference indices on average. Across 36 schemes, the average decline stood at 8.23 per cent, much lower than the double-digit fall seen in most equity PMS categories. However, that was still worse than the NSE Multi Asset Index 1’s 6.45 per cent decline and the NSE Multi Asset Index 2’s 6.88 per cent fall. Only 10 schemes beat Index 1, while 12 outperformed Index 2.

That makes the category’s March showing slightly mixed. On an absolute basis, multi-asset strategies did their job better than pure equity portfolios by cushioning losses through diversification. But on a relative basis, a majority of managers were unable to keep pace with the multi-asset benchmarks, suggesting that asset allocation or security selection did not work as effectively as expected during the month’s market stress.

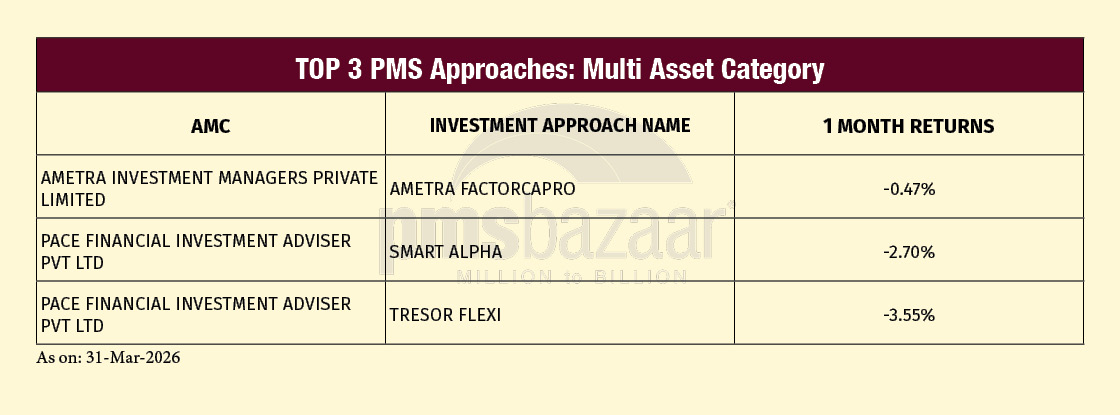

At the top end, though, some strategies stood out sharply. Ametra Investment Managers’ Ametra FactorCapro was the best-performing multi-asset PMS, falling just 0.47 per cent. Pace Financial’s Smart Alpha and Tresor Flexi followed with declines of 2.70 per cent and 3.55 per cent respectively

That suggests the category offered meaningful downside protection at the top end, even if the average manager did not fully deliver on benchmark-relative defence. March reinforced the central appeal of multi-asset PMSes: they may not eliminate losses in a broad sell-off, but they can materially reduce the drawdown compared with pure equity strategies.

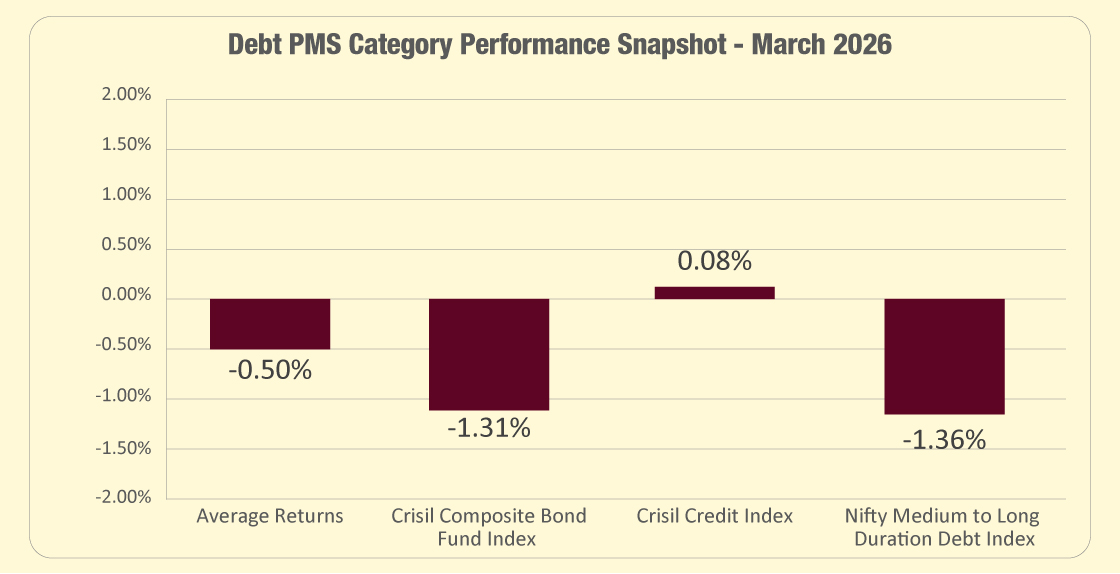

Debt PMSes emerge as March’s clear relative winners

Debt PMSes were by far the most resilient category in March 2026. Across 17 schemes, the average return stood at minus 0.50 per cent, a far smaller decline than any equity or multi-asset PMS segment. The category also compared well against most of its relevant benchmarks. Fourteen schemes outperformed the CRISIL Composite Bond Fund Index, which fell 1.31 per cent, and an equal number beat the Nifty Medium to Long Duration Debt Index, which declined 1.36 per cent. Against the CRISIL Credit Index, which rose 0.08 per cent, 11 schemes managed to do better.

That benchmark pattern needs a little care in interpretation. Debt PMSes did not beat every debt benchmark uniformly because credit-oriented indices held up better than duration-heavy ones during the month. Even so, the broad message is clear: fixed-income portfolios offered far superior capital protection than risk assets during March’s market turbulence.

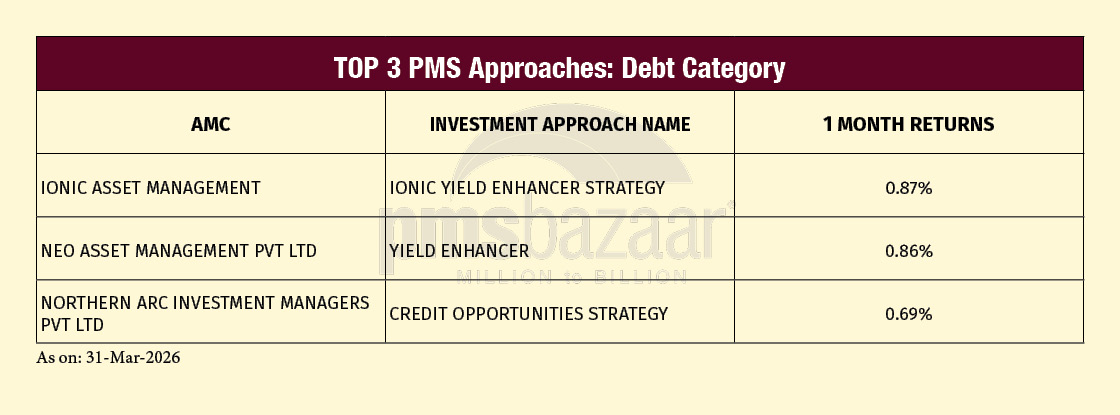

At the top of the table, several debt PMSes delivered outright positive returns. Ionic Asset Management’s Ionic Yield Enhancer Strategy led the category with a gain of 0.87 per cent, followed closely by Neo Asset Management’s Yield Enhancer at 0.86 per cent. Northern Arc’s Credit Opportunities Strategy returned 0.69 per cent.

That stands in sharp contrast with equity PMSes, where even top-ranked schemes often remained in negative territory. March therefore reinforced a basic but important point: in phases of broad market stress, debt PMSes may not offer headline-grabbing upside, but they can play a crucial role in preserving capital and stabilising portfolios.

Outlook for April-2026

For PMS investors, the recent correction may be creating a more constructive entry environment than the headlines suggest. Valuations across large-, mid- and small-cap stocks have already corrected sharply from their September 2024 highs, which means a meaningful part of the war-related risk may now be reflected in prices. While markets could remain headline-driven in the near term, the sharp fall has improved the risk-reward balance for investors with a medium- to long-term horizon.

The key risk, of course, would be a longer or more intense/complicated conflict. But if that does not materialise, India appears relatively well placed to absorb short-term shocks. Strong domestic demand, policy agility and continued government capex should help support growth, while a stabilising rupee is also a positive. If export prospects improve and corporate profit growth returns to early double digits, active managers could find better stock-picking opportunities after this correction. For PMS investors, that strengthens the case for staying focused on portfolio quality, manager discipline and long-term allocation rather than reacting to near-term volatility.

Happy Investing

Recent Blogs

Early-Stage Access to India's Manufacturing Growth Story

PMS Bazaar recently organized a webinar titled “Early-Stage Access to India's Manufacturing Growth Story,” which featured Mr. Vignesh Shankar, Founder & Managing Partner, a99 VC. This blog covers the important points shared in this insightful webinar.

May sees selective alpha as PMSes navigate market consolidation

Despite a subdued market environment, PMS strategies continued to deliver positive returns. Leadership remained concentrated in Thematic, Small Cap and Small & Midcap categories, underscoring the value of active management and focused portfolio positioning.

SEBI’s Accredited Investor Certificate: Exclusive Access to AIFs, PMS, SIFs & Private Markets

PMS Bazaar recently organized a webinar titled “SEBI’s Accredited Investor Certificate: Exclusive Access to AIFs, PMS, SIFs & Private Markets,” which featured Mr. Rajesh Kumar S, Head of Business, NSDL Database Management Limited. This blog covers the important points shared in this insightful webinar.

April rebound lifts PMS strategies, but small-cap tilt drives leaders

A broad market recovery helped managers beat large-cap indices, though alpha against wider benchmarks remained more selective and category-dependent

SEBI’s GARUDA Framework: A Big Boost for India’s AIF Industry and GIFT City Ecosystem

India’s Alternative Investment Fund (AIF) industry has evolved rapidly over the last few years. Investors today are increasingly moving beyond traditional investment products such as mutual funds and fixed deposits in search of differentiated opportunities across Private Equity, Venture Capital, Private Credit, Real Estate, infrastructure, and Category III long-short strategies.

Winners & Losers: Sectors to Watch in the Current Global Crisis

PMS Bazaar recently organized a webinar titled “Winners & Losers: Sectors to Watch in the Current Global Crisis,” which featured Mr. Arpit Shah, Co-Founder and Director, Care Portfolio Managers. This blog covers the important points shared in this insightful webinar.

Why Market Corrections Are the Best Time to Build Your Core Equity Portfolio

PMS Bazaar recently organized a webinar titled “Why Market Corrections Are the Best Time to Build Your Core Equity Portfolio,” which featured Mr. Amit Nigam, Deputy CIO, ASK Investment Managers. The webinar blog covers insights from Mr. Nigam, which includes explanation how recent stock market volatility in India creates opportunities for long-term investors. It highlights shifting from a fixed deposit mindset to equities, his blog covers the important points shared in this insightful webinar.

Why ETF-Only Portfolios Are the Most Tax-Efficient Way to Invest

How deferred taxation and lower LTCG rates compound into significantly higher post-tax wealth for long-term investors